Most van lifers are unaware of the insurance gaps that could leave them financially devastated in the event of a total loss. Standard auto insurance policies aren’t designed for individuals who live full-time in their vehicles.

The coverage shortfalls can result in tens of thousands of dollars in costs when disaster strikes. We learned this the hard way, losing $87,000 in personal belongings and facing months of uncertainty while fighting for proper compensation.

In this article, you’ll discover the real-world insurance lessons we learned from our total loss, the specific coverage types every van lifer needs, and actionable steps to properly protect your mobile lifestyle investment.

If you’re planning your first van conversion or you’ve been on the road for years, comprehending van life insurance and RV insurance requirements could save you from the financial and emotional devastation we experienced.

Van Life Insurance DISASTER: Critical Mistakes That Cost This Couple Everything

Van Lifers Lost Everything in Fire – Here’s What They Learned About Insurance

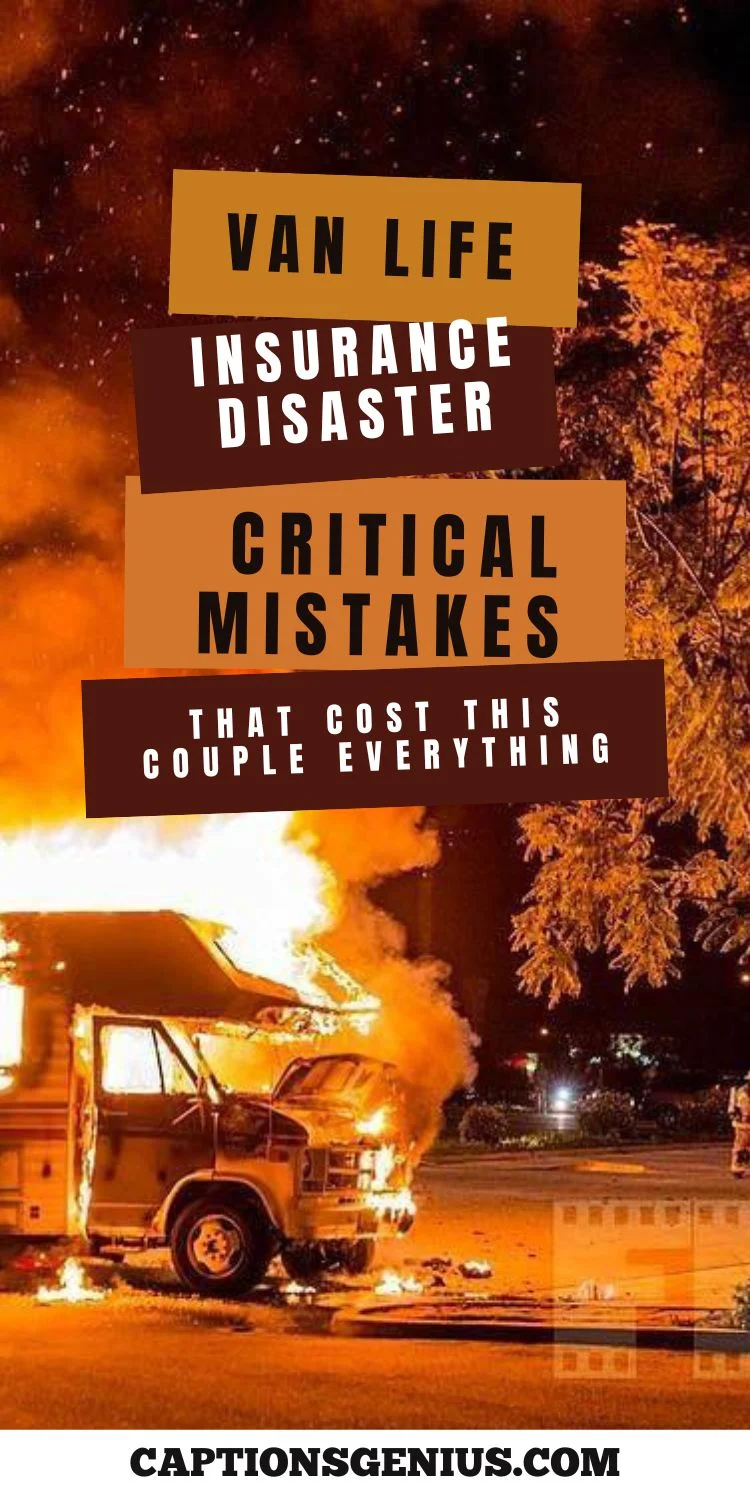

At 2 AM on a Tuesday in Montana, Mark and Sarah woke up to the smell of smoke and had exactly 90 seconds to escape their burning van with nothing but the clothes on their backs.

As they watched three years of careful conversion work and everything they owned disappear into flames, they thought their comprehensive insurance would cover them. They were devastatingly wrong.

They learned this the hard way, losing $87,000 in personal belongings and facing months of uncertainty while fighting for proper compensation.

This article reveals the real-world insurance lessons they learned from their total loss, the specific coverage types every van lifer needs, and actionable steps to properly protect mobile lifestyle investments.

If you’re planning your first van conversion or you’ve been on the road for years, understanding van life insurance and RV insurance requirements could save you from the financial and emotional devastation they experienced. Don’t make the same costly mistakes they did; your mobile lifestyle protection depends on getting this right before it’s too late.

The Night Their Mobile Home Burned Down

The smoke alarm screaming at 2:07 AM wasn’t part of any dream. The electrical fire had started behind their custom-built kitchen cabinets and spread fast.

They grabbed their phones and stumbled outside in their underwear. The flames were already shooting through the roof. In less than four minutes, their entire mobile home became a towering inferno that lit up the Montana wilderness like a giant torch.

The volunteer fire department arrived 18 minutes later. But it was too late. They could only watch it burn and make sure the grass fire didn’t spread. By dawn, all that remained was a charred metal skeleton and piles of melted plastic where their home used to be.

Here’s what Mark and Sarah lost in that van fire:

i. Custom kitchen build-out: $18,000

ii. Solar power system and batteries: $12,000

iii. Laptop computers and camera gear: $15,000

iv. Clothes, books, and personal items: $22,000

v. Climbing gear and outdoor equipment: $8,000

vi. Van modifications and upgrades: $12,000

Total loss: $87,000

The Red Cross put them up in a motel for three nights. They had no clothes except what strangers donated. No transportation. No home. And they were about to learn that their insurance claim would be the start of their real nightmare.

The emotional hit almost broke them. People don’t realize how much of their identity is tied to their stuff until it’s all gone. That van wasn’t just transportation; it was their home, their office, their everything. Losing it felt like losing themselves.

Their First Insurance Mistake – Why “Full Coverage” Wasn’t Enough

They called their insurance company from the motel parking lot. The agent was polite but delivered crushing news: their comprehensive coverage would only pay $1,200 for personal property.

Twelve hundred dollars. For $87,000 worth of belongings. “But they have full coverage,” Sarah said, her voice breaking. The agent explained that standard auto insurance covers vehicles, not the contents inside. Their “comprehensive coverage” was designed for people who drive their cars to work, not people who live in them full-time.

Here’s where most van lifers get blindsided. Auto insurance treats vans like cars, even if people spend $80,000 converting them into homes. The insurance company sees:

i. Vehicle value: $45,000 (covered)

ii. Personal property: $1,200 limit (barely covered)

iii. Custom build-out: $0 (not covered at all)

Standard auto insurance personal property limits range from $500 to $1,500. That might cover a gym bag and some jumper cables in a regular car. But not a van conversion.

Mark and Sarah thought their State Farm agent understood their situation when they bought the policy. They said they lived in the van full-time. They described their conversion. But the agent just sold them regular auto insurance with comprehensive coverage. It was a big mistake.

RV insurance for van conversion costs about 20% more than auto insurance. But it can save van lifers tens of thousands of dollars when disaster strikes. The average van conversion costs between $60,000 and $120,000, according to Outside Magazine. Regular auto insurance won’t come close to covering that investment.

Industry data shows that 78% of van lifers have inadequate insurance coverage for their actual lifestyle and possessions. Most people assume their auto insurance will cover them. Most people are wrong.

Their “comprehensive coverage” covered the van’s book value but ignored everything that made it their home. Custom cabinets, solar panels, water systems, and personal belongings got zero coverage under their auto policy.

What Van Life Insurance Covers (And Why Van Lifers Need It)

Real van life insurance is completely different from auto insurance. It’s designed for people who live in their vehicles, not just drive them on weekends.

Specialized RV Insurance vs. Standard Auto Insurance:

Standard auto insurance covers people like commuters. RV insurance covers people like homeowners who happen to live on wheels. The difference is huge.

With proper nomad insurance, van lifers get:

Full-Timer Insurance Endorsements: This covers people when the van is their primary residence, not just a weekend toy. It includes liability coverage for when they’re parked and living in the van, plus coverage for accidents that happen while they’re “at home.”

Personal Effects Coverage: Instead of $1,200, van lifers can get $30,000 to $100,000 in personal property coverage. This covers laptops, cameras, clothes, kitchen gear, and everything else they own.

Temporary Living Expenses: When mobile homes burn down, people need somewhere to live. This coverage pays for hotels, food, and transportation while they figure out their next move. Mark and Sarah ended up spending $8,000 out of pocket on hotels and rental cars that proper RV insurance would have covered.

Emergency Expense Coverage: Towing a burned-out van costs serious money. So does storing the wreckage while the insurance company investigates. Emergency coverage handles these costs that can easily hit $5,000 or more.

Replacement Cost Coverage: This pays to replace belongings at today’s prices, not what people paid five years ago. A laptop might be worth $500 used, but replacement cost coverage will buy a new $2,000 laptop.

Full-Timer Coverage Benefits:

Here’s what proper RV insurance costs compared to the protection it provides:

i. Basic RV insurance: $1,200-$1,800 per year

ii. Full-timer endorsement: Additional $300-$600 per year

iii. Personal property coverage ($50,000): Additional $200-$400 per year

iv. Total annual cost: $1,700-$2,800

Compare that to Mark and Sarah’s $87,000 loss. Proper insurance would have cost them about $2,000 per year but saved them $85,000 in out-of-pocket costs.

Claims processing with RV insurance also works better for nomads. Auto insurance adjusters don’t understand van conversions. RV insurance adjusters deal with custom living spaces every day. They know how to value solar systems, custom cabinetry, and mobile office setups.

The average RV insurance claim gets processed in 30-45 days. Auto insurance claims for unusual situations like van fires can drag on for months because the adjusters don’t know how to handle them.

The Hidden Costs They Don’t Tell Van Lifers About

Even with good insurance, a total loss hits people with surprise costs that nobody warns them about. These hidden expenses nearly bankrupted Mark and Sarah during their insurance claim.

Replacement Cost vs. Actual Cash Value:

A three-year-old laptop is worth maybe $400 on the used market. But replacing it costs $1,200. If van lifers don’t have replacement cost coverage, they get the $400. Good luck buying a $400 laptop that can handle work.

Their camera gear was worth $15,000 new but only $6,000 used. Without replacement cost coverage, they would have gotten the $6,000 and been unable to replace their business equipment. That’s how people lose their livelihoods along with their homes.

Custom Build-Out Depreciation:

Insurance companies love to depreciate custom work. A beautiful $20,000 kitchen build-out? They’ll say it’s worth $8,000 after three years. A solar system? Half value after two years, even though it works perfectly.

Mark and Sarah had to fight for eight months to get proper compensation for their custom work. The insurance company initially offered them $12,000 for build-outs that cost $35,000. Only after hiring a public adjuster did they get a fair settlement.

The Costs Nobody Mentions:

Storage fees for the burned van: $1,200. Towing the wreckage: $800

Hotel costs during the claim: $6,400 Rental car for two months: $3,200 Eating restaurant food: $2,800 Replacing immediate necessities: $1,900 Public adjuster fee: $4,200 Total out-of-pocket: $20,500

And that’s with insurance coverage. Without proper van conversion value protection, these costs would have been much higher.

For digital nomads, there’s another hidden cost: lost income. When mobile offices burn down, people can’t work. Mark and Sarah lost about $15,000 in income during the two months it took to get back on their feet. Nomad business insurance can cover some of this, but most people don’t even know it exists.

Hotel costs for displaced van lifers average $150-200 per night, according to Good Sam. If claims take 60 days to settle, that’s $9,000-$12,000 just for a place to sleep.

How to Protect Van Life Investments

Getting proper van life insurance takes more work than buying auto insurance, but it’s not complicated. Here’s exactly how to do it right.

Choose the Right Insurance Provider:

Not all insurance companies understand van life. Van lifers need providers that specialize in RVs and alternative lifestyles. The top RV insurance providers for van life are:

- National General (Good Sam): Best for full-timers, excellent customer service

- Progressive: Good rates, decent coverage options

- Geico: Competitive pricing, limited full-timer options

- GMAC: Strong coverage, higher premiums

- Foremost: Specializes in unique situations

Van lifers should avoid regular auto insurance companies. They don’t understand mobile lifestyle needs and will leave people exposed.

Document Everything Before Needing It:

Insurance companies want proof of what people owned and what it cost. Van lifers should start documenting now:

i. Photos of every room and storage area

ii. Video walkthrough of the entire van

iii. Receipts for all conversion work and major purchases

iv. Professional appraisal of custom build-out work

v. Serial numbers for electronics and appliances

vi. Before and after photos of any modifications

Store this documentation in the cloud, not just in the van. Mark and Sarah lost all their receipts in the fire and had to reconstruct everything from memory and bank statements.

Calculate Coverage Amounts That Work:

Don’t guess at coverage amounts. Calculate what’s needed:

Personal Property: Add up everything owned. Include clothes, electronics, kitchen gear, tools, books, everything. Most full-time van lifers need $40,000-$80,000 in personal property coverage.

Van Value: Get a professional appraisal if major conversion work has been done. The insurance company needs to know the van is worth more than its book value.

Temporary Living: Budget $200 per day for hotels and food. If claims might take 60 days, get at least $12,000 in temporary living coverage.

Important Policy Endorsements to Add:

- Full-timer endorsement (mandatory if living in the van)

- Replacement cost coverage (worth every penny)

- Emergency expense coverage (covers towing and storage)

- Personal liability (protects when parked)

- Vacation liability (covers at campsites)

Review Policies Every Year:

Van life insurance needs change as people add equipment and modify their setups. Review policies annually and update coverage amounts. Add new equipment to the documented inventory right after buying it.

The key is working with an agent who understands mobile lifestyle coverage. Don’t try to buy van life insurance tips online. Talk to a human who specializes in RV insurance and can explain options.

Red Flags That Will Get Claims Denied

Insurance companies look for reasons to deny claims. Van lifers should avoid these mistakes that can void coverage completely.

Don’t Lie About How Vans Are Used:

The biggest van insurance mistake is misrepresenting living situations. If people live in their vans full-time but tell the insurance company it’s for weekend camping, their claims will get denied.

Insurance fraud is a felony. But more notably, it doesn’t work. Insurance companies analyze major claims. They’ll find out if people lied about their living situations, and they’ll use it to deny entire claims.

Be honest about:

- How many days per year do people live in the van

- Where do they park it (some policies exclude urban camping)

- What they use it for (living vs. recreation)

- How many people live in it full-time

Inadequate Personal Property Coverage:

Most people buy too little personal property coverage because they don’t want to pay higher premiums. This is penny-wise and pound-foolish.

If van lifers own $60,000 worth of belongings but only carry $20,000 in coverage, they’ll eat the $40,000 difference. The extra premium for proper coverage is maybe $300 per year. One claim pays for decades of higher premiums.

Skip the Professional Appraisal:

If people have spent more than $40,000 on their conversion, they should get a professional appraisal. This document shows the van’s true value and prevents arguments during claims.

Professional appraisals cost $400-$800 but can save tens of thousands if there’s a total loss. The insurance company can’t argue with a certified appraisal from a qualified professional.

Not Updating Coverage After Modifications:

Every time people add equipment or modify their vans, they should update their insurance policies. That new $8,000 solar system isn’t covered unless they tell their insurance company about it.

Most people forget to update their policies and discover coverage gaps during claims. Don’t learn this lesson the hard way.

Choosing Cheap Insurance Without Reading the Fine Print:

The cheapest policy is rarely the best value. Low premiums usually mean coverage gaps that will cost big money during claims.

Industry data shows that 23% of RV insurance claims get denied due to coverage gaps or misrepresentation. Don’t become a statistic because of wanting to save $500 per year on premiums.

Van lifers should read their policies. Understand what’s covered and what isn’t. Ask questions. The few hours spent understanding coverage could save them from financial disaster.

How Mark and Sarah Rebuilt Their Life After the Fire

Six months after the fire, Mark and Sarah had a new van and a completely different approach to insurance and emergency planning. Here’s what they learned about recovery and what they’d do differently.

Their New Insurance Strategy:

They switched to National General RV insurance with full-timer coverage. Their new policy costs $2,400 per year but includes:

- $75,000 personal property coverage (replacement cost)

- $15,000 temporary living expenses

- $10,000 emergency expenses

- Professional liability coverage for their business

- Vacation liability coverage

The higher premium hurts every month. But it’s nothing compared to the $85,000 they lost because of inadequate coverage.

Emergency Preparedness Improvements:

They now keep a “go bag” with essentials that they can grab in 30 seconds:

- Copies of all important documents

- Emergency cash ($2,000)

- Basic medications

- Phone chargers and a backup battery

- Change of clothes for both of them

They also store complete documentation in three places: cloud storage, physical copies at Sarah’s parents’ house, and a fireproof safe in the van.

Financial Recovery Timeline:

Months 1-2: Living in hotels, fighting with insurance.

Months 3-4: Finding and buying a replacement van

Months 5-6: Basic conversion to make it livable.

Months 7-12: Completing the build-out and replacing belongings.

Months 13-18: Full financial recovery

The insurance settlement took eight months and required hiring a public adjuster. Even with professional help, they never recovered the full $87,000 loss.

Emotional Recovery:

Losing everything changes people. Mark and Sarah are more careful now, but also more grateful for what they have. The fire taught them that stuff is just stuff, but it also showed them how much van life insurance lessons learned can protect financial futures.

The hardest part wasn’t losing their belongings. It was losing their sense of security. For months after the fire, they’d wake up sniffing for smoke. They installed extra fire detection systems and escape routes that they practice regularly.

Mobile lifestyle resilience means being prepared for disasters but not living in fear of them. Good insurance gives people the confidence to enjoy van life without constantly worrying about what could go wrong.

Don’t Make Their Expensive Mistakes

Mark and Sarah’s van fire cost them $87,000 in belongings and nearly destroyed their mobile lifestyle dreams. But it taught them insurance lessons that could save others from the same financial disaster.

The key insurance lessons that matter most:

i. Standard auto insurance won’t protect van life investments

ii. Full-timer coverage is mandatory if people live in their vans

iii. Personal property coverage should match what people own

iv. Professional appraisals prevent arguments during claims

v. Replacement cost coverage is worth every penny

Mobile homes are the biggest investments and most important possessions for van lifers. Don’t protect them with insurance designed for weekend warriors.

Get proper van life insurance protection before needing it. Talk to an RV insurance specialist who understands mobile lifestyles. Document belongings while still owning them. And be honest about how vans are used.

The peace of mind that comes with proper nomad peace of mind coverage is worth far more than the extra premium cost. Don’t learn this lesson the hard way like Mark and Sarah did.

Van life adventures are just beginning for many people. Make sure they’re properly protected so one bad night doesn’t end them forever.